The Rockefeller Method for Building and Passing on Generational Wealth

The Rockefeller Method ensures your financial legacy lasts, whether you leave $1 million or $100 million. This method focuses on passing wealth and values, opportunities, and empowerment to future generations.

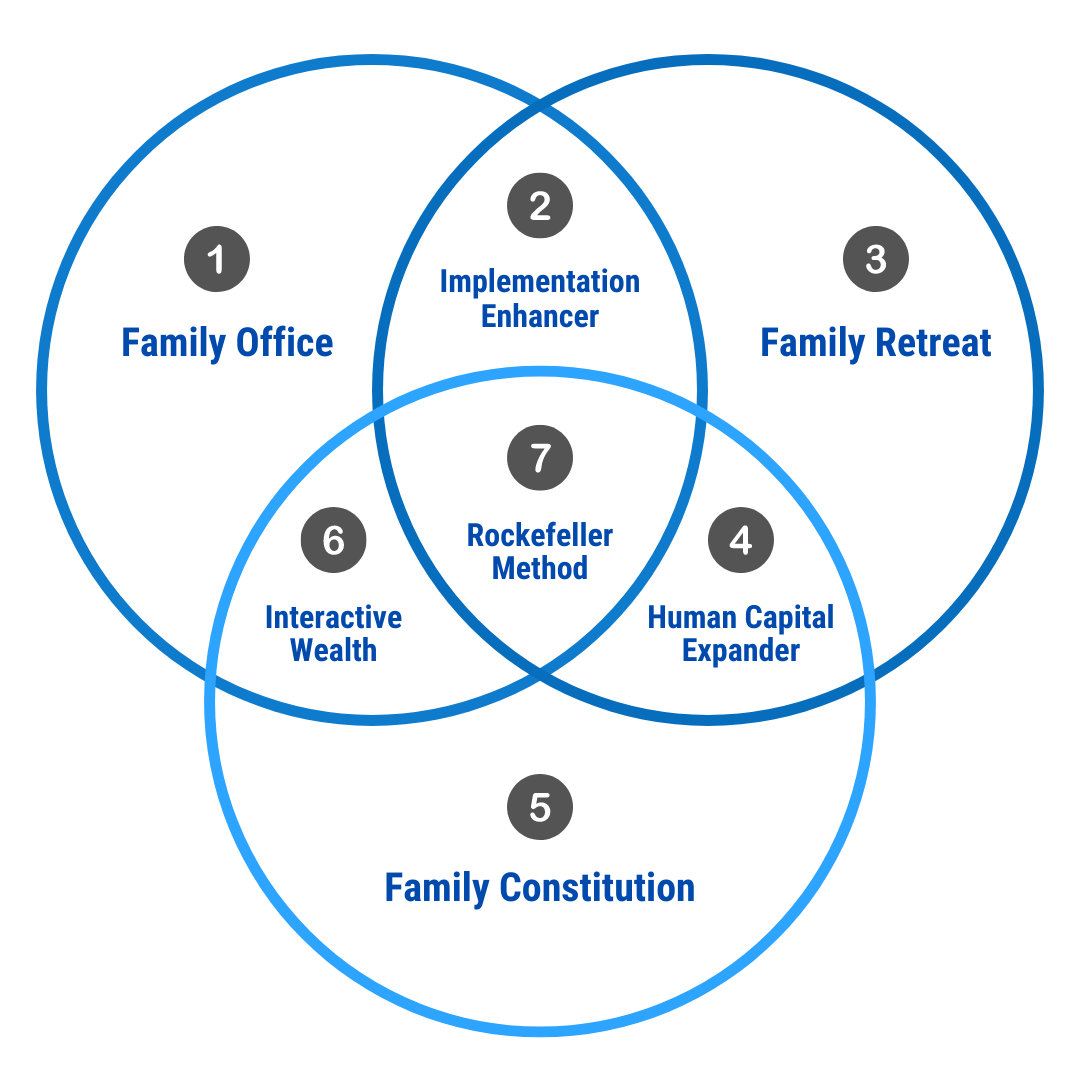

Family Legacy Rings

The Rockefeller Method centers on the "Family Legacy Rings," which include:

Family Office

Family Retreat

Family Constitution

These rings create a structure to perpetuate your legacy beyond monetary wealth.

The Family Office

The Rockefellers have maintained their wealth for six generations and counting, in part because they have a dedicated financial team called a Family Office.

You can replicate this with a fractional or virtual Family Office, integrating financial professionals who work together for your family. This prevents the risks of siloed financial management and ensures cohesive financial planning.

The Family Retreat

Regular family meetings and retreats foster trust, structure, and traditions. These gatherings help transfer values and philosophies to your heirs, ensuring they understand and uphold your legacy.

The Family Constitution

A Family Constitution acts like a preamble to your trust. It uses incentive-based planning and a board of trustees to ensure your heirs benefit when they are wise stewards of the resources provided.

The Rockefeller Method

The Rockefeller Method is a specific trust that owns your specially designed, optimally funded life insurance contract on you and your family members. It includes asset protection and uses trusts to enact your plan to empower your heirs for generations.

If you have a trust, you can keep your assets private, avoid probate, minimize tax, and have provisions that “keep the money together”—and the family. Without a trust or even with a boilerplate trust, you can count on the default outcome of “divide, distribute, and destroy,” just as in the Vanderbilt family.

If your assets go through probate, the court will make the choice, not you. And it will be public knowledge; all that you have or do not have will be on display. With a trust, you can “own nothing, control everything”: a core mantra of the Rockefeller family.

You can make it so your heirs don’t have to start over at zero with every generation but instead can leverage your legacy to support their passion and purpose and live lives they love.

For example, if your descendants have a business idea, you may want to empower them to start that business with the family trust rather than leaving them to try and make it happen while working jobs. You may want to help your kids pay for their education so they aren’t shackled with debt.

In the Rockefeller Method, you use a trust to protect and perpetuate your wealth and utilize optimally funded whole life insurance to fund the trust from generation to generation.

It is a way to store your money without having to worry about market loss. It is a banking alternative that gives you stability, security, and liquidity.

The financial structure is supported by a legacy structure of values and vision. The financial strategy and the centerpiece that protects your economic value, today and in the future, is a properly structured, optimally funded whole life insurance policy with a participating mutual company.

Leave a Legacy

Whole Life Certified experts know the core of this methodology and have used it to power the Rockefeller Method.

Properly structured, optimally funded whole life insurance is the strategy for maximizing the tool of life insurance. It doesn’t work because of the product; it works because of the strategy of looking cohesively and comprehensively at how things work together.

Your overall financial blueprint is the key to guiding your financial choices. Insurance is only one piece of the puzzle, albeit an important one.

But what does legacy mean to you? Legacy is the total impact of the thoughts, ideas, values, signposts, examples, and influence we leave to those we love.

Legacy includes not just the money we leave, but more importantly, the lessons and instructions that come with that money. Legacy is our values, our actions, and our love passed down through generations.

How Whole Life Insurance

Fuels the Method

With the Rockefeller Method, as soon as a beneficiary of your trust is born, the trust takes out a whole life policy for them and for the maximum amount of insurance the company will offer. That way, if an heir borrows money from the trust but isn’t able to pay it back, it’s not detrimental to the survival of the trust.

It is also important to have a death benefit to replenish funds in case tax fluctuations, inflation, or economic turmoil create losses within the trust.

There can be safeguards, such as restrictions on how much an heir can borrow and ensuring that if they are unable to pay it back in full, the trust will be made whole again by the life insurance. And when an heir does pay back a loan, the interest is NOT paid to the government or a banking institution, but back into the family trust, keeping the family strong.

You can set up a trust like this for experiences, entrepreneurship, and any number of enterprises. You can structure it so that people can only borrow a certain amount or even a specific number of times, depending on the assets in the trust.

Manage Your Trust with a Board of Directors

An extended family mission statement that will help govern their decisions and make sure the money is put to good use. The board is a group of people you select that will best represent you in case of death. The board can help educate, mentor, and support the family while also protecting your wealth.

The Family Constitution allows for more dynamic management in an ever-changing, unpredictable future. It is governed by principles, values, and frameworks to inform decisions that will impact heirs. It gives enough structure, but not so much detail that it may be rendered irrelevant by technological advances and change.

© Copyright 2025 | Ripwater LLC | All Rights Reserved